The post First Home Savings Account (FHSA) appeared first on Virtus Group.

]]>Suppose you’re looking to enter the market for the first time. In that case, you will want to use every resource available, including government programs, professional guidance, or preferably both. Knowledge is power, and several programs are available to help you reach your goals.

Available Programs

- First-Time Home Buyer Incentive

- Home Buyer’s Plan

- Home Buyer’s Amount

- Land Transfer Tax Refund

- First Home Savings Account

If you want to discuss how you or someone you know can use the above programs, talk with your financial planner about which options may be right for you. The focus of this publication is to provide additional information on the First Home Savings Account (FHSA).

Tax-Free First Home Savings Account (FHSA)

FHSA is a proposed savings account that acts like an RRSP, specifically for those saving to purchase their first home.

Quick Facts

- You must be 18 years of age and a Canadian resident to open an FHSA.

- Contributions are tax-deductible, like an RRSP.

- Withdrawals, including accrued investment income or gains, are tax-free, like a TFSA, if the withdrawal is used to purchase a home.

- Your maximum tax-deductible contribution will be $8,000 per year, lifetime maximum of $40,000.

- Upon the fifteenth anniversary of opening an FHSA or when the individual turns 71 years old – whichever event occurs first – the account will be closed. Any savings not used towards the purchase a qualifying home could be transferred into an RRSP or RRIF on a tax-free basis or would otherwise have to be withdrawn on a taxable basis.

Eligibility

- You qualify as a First-Time Home Buyer as per the definition below

- Can be used with other programs

First Time Home Buyer Definition

First, you need to clarify if you are, in fact, a First-Time Home Buyer. In Canada, a First-Time Home Buyer is someone who has yet to own a home in which they lived at any time during the part of the calendar year before the account is opened or at any time in the preceding four calendar years. In addition, the individual must not have occupied a home owned by their current spouse or common-law partner.

Other Pertinent Details

The type of investments eligible to be held in an FHSA follow the same criteria as those permitted within a TFSA. Generally, publicly traded securities, governments and corporate bonds, mutual funds, and guaranteed investment certificates are permitted to be held within an FHSA. On the other hand, investments such as non-arm’s length companies, land, shares of private corporations and general partnership units are not permitted to be held within an FHSA.

The annual contribution limit of $8,000 allows for a tax deduction for contributions to an FHSA in a calendar year. However, unlike an RRSP, contributions within 60 days of the following calendar year cannot be deducted against the prior year’s income.

Undeducted contributions carry forward

Like an RRSP, an individual is not required to claim a deduction in the year contributions are made –

undeducted contributions can be carried forward indefinitely and deducted in a future year. Consult with your accountant or advisor to determine the best strategy for optimizing the deduction of FHSA contributions.

The unused portion of the $8,000 annual limit can be carried forward into the future. However, the maximum contribution room to be carried forward is capped at $8,000. An individual can hold multiple FHSAs. Regardless, the total annual contribution limit of $8,000 and a lifetime limit of $40,000 applies across all accounts.

Individuals can transfer funds, on a tax-free basis, from an RRSP to an FHSA, subject to the FHSA above mentioned limits and qualified investment rules. These transfers would not be deductible and would not reinstate an individual’s RRSP contribution room. Overcontributions to an FHSA would be subject to a 1% tax based on the highest amount of such excess each month that the individual remains in an overcontributed position.

If an individual passes away while holding an FHSA, their spouse should be named as the successor account holder to allow the transfer of the FHSA on a tax-exempt basis to the spouse, provided the spouse meets the criteria to hold an FHSA.

The post First Home Savings Account (FHSA) appeared first on Virtus Group.

]]>The post Individual Pension Plan (IPP) appeared first on Virtus Group.

]]>How an Individual Pension Plan (IPP) works

An IPP is a tax-deferred savings vehicle used to invest and save for retirement. Contributions are tax-deductible and made directly from the corporation. Similar to an RRSP, the assets inside an IPP are tax-deferred until withdrawn, at which time they are treated as income.

How much can be contributed to an Individual Pension Plan?

| Age | RRSP Contribution | IPP Contribution | IPP Advantage | |

| 45 | $30,780 | $33,200 | $ 2,420 | 8% |

| 50 | $30,780 | $36,400 | $ 5,620 | 18% |

| 55 | $30,780 | $40,000 | $ 9,220 | 30% |

| 60 | $30,780 | $43,900 | $13,120 | 43% |

| 65 | $30,780 | $48,300 | $17,520 | 57% |

Who is a good candidate for an Individual Pension Plan?

- Business owner

- Registered professional

- Middle aged adult (40+)

- T4 Earnings of $100K+

- An IPP can be established for someone with lower earnings

Case Study

A business owner, aged 55, incorporated for 24 years, maximum T4 earnings of $178,600 with a current RRSP balance of $291,866.

- $156,600 in immediate past service funding,

tax-deductible to the company - $221,700 in qualifying transfer (from existing RRSP balance)

- Up to $446,211 more in tax-deductible contribution room over working years (excluding past service)

- The IPP balance could be up to $1,306,700

more than the RRSP balance

All the above figures are based on 2022 prescribed assumptions.

Advantages of an Individual Pension Plan

- Increased tax-deductible contribution room – up to 65% more than an RRSP

- Can reduce passive income in corporation

- Tax-deductible company contributions for prior years (past service)

- Richest benefit plan in Canada – 2% defined benefit pension plan

- All costs are tax-deductible to the company

- Creditor protection

- Increased corporate and personal tax savings

- Can include employed family members and pass on wealth to the next generation

The post Individual Pension Plan (IPP) appeared first on Virtus Group.

]]>The post The Psychology of Selling Your Business appeared first on Virtus Group.

]]>You may have invested so much time and energy into your business that it’s become a part of you. Or there are family issues that are holding you back. Whatever the reason, it’s essential to recognize that this reluctance is not uncommon, and it’s perfectly normal to feel this way.

You may find yourself delaying the acceptance of a fair offer, stalling the process, declining, or otherwise sabotaging the deal without really understanding why. You may think it just didn’t “feel right”, the buyer wasn’t the right fit, or you convince yourself you’re not ready. Perhaps it is one of these reasons, but often this is not the case.

The psychology of selling your business

Selling a business that has been painstakingly created, nurtured, and struggled with, and one that is ultimately successful, is akin to a child leaving home to take on the world for themselves. For owners like you, a business can be like having a child. Whether you’ve conceived the business from an idea, inherited the family business, or purchased an established enterprise, you’ve put your blood, sweat, and tears into your business to make it successful.

Like new parents, you can often feel nervous, unprepared, and overwhelmed, having never done this before. Regardless, you push through as the reward and satisfaction far outweigh the fear; the effort is fulfilling and long-lasting. Over the years, you’ve spent many hours cultivating and nurturing the business, celebrating its successes, and watching it grow into a successful, independent, self-reliant enterprise that is ultimately valuable to the world.

You and your business struggled together, overcame obstacles in the face of adversity, stumbled, got back up, and learned and grew through it all. Like a baby, you initially carried the business when it could not carry itself. Over time, your business grew and found its legs and rhythm. As your business matured, it became important to others – clients, staff, suppliers, and, most importantly, you. Like a child, the business gained independence over time and needed you less and less, becoming an entity unto itself. You no longer manage every aspect of the enterprise, coddle it, and protect it. Your business has become a thriving entity that can stand on its own.

Letting go of what you or your family created, nurtured, and grew is often very difficult. Like a child, you are proud of what it has become but still worry about what might happen if you let it go. Will it be okay without you? Will it be damaged if you are not there to protect it? Will it even survive if you are not guiding it in the future?

With business, as with children, you reach the point where you have done everything you can to prepare it for the world, and you must let go. Let it move on. Let it continue its evolution, whatever that may be.

Considering a different perspective about the sale of your business and understanding the emotions you may be experiencing often helps you conquer the reluctance of finalizing the sale. Selling is a very difficult time for many business owners, which could result in a lost opportunity to monetize your lifelong achievements if you can’t overcome this obstacle.

How we can help

Work with your trusted accounting and financial advisors under our TriCert integrated approach. We specialize in owner-managed businesses to help you overcome many psychological hurdles of selling your business.

integrated approach. We specialize in owner-managed businesses to help you overcome many psychological hurdles of selling your business.

Leveraging the experience of accountants and tax specialists, and integrating these advisory services with your financial planner, can give you the peace of mind and the confidence to work through one of the most significant events in your lifetime with a strong team supporting you every step of the way.

The post The Psychology of Selling Your Business appeared first on Virtus Group.

]]>The post Staying Calm When Markets are Volatile appeared first on Virtus Group.

]]>In times of economic turbulence, it’s normal to feel apprehensive when you’re about to read your portfolio’s performance. And, of course, seeing the fluctuating short-term results doesn’t help. It is more important to keep your sights on the bigger picture and stay focused on your long-term investment strategy and performance. By doing so, you can navigate the choppy waters of the current economic climate more confidently and ultimately achieve your financial goals.

Typically, volatility is a short-term issue; in the long run, your long-term investment plan and confidence in your investment holdings matter. Therefore, avoiding short-term “noise” can be a good strategy. While performance is undoubtedly crucial, it should be evaluated in years, not months.

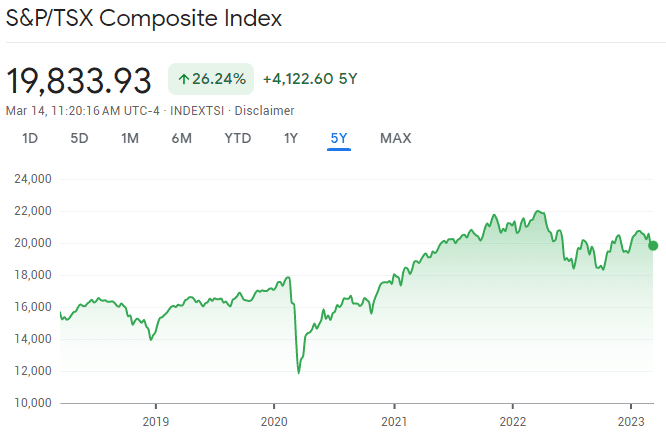

For example, take a look at it in graph terms:

The short-term view

S&P/TSX Composite Index down 6.36% over the past 1 year

The long-term strategy

S&P/TSX Composite Index up 26.24% over the past 5 years

Strategies for navigating market volatility

The performance figures can be an unpleasant surprise, depending on the period you are looking at or the duration being reported on your account statements.

Consider:

- Evaluating the quality and long-term sustainability of your investments with your portfolio manager. It’s likely that your holdings are still reasonable, and no drastic changes are necessary. You may come across opportunities to refine your portfolio, but try to refrain from making significant “panic changes” that could lead to missing out on future market recoveries.

- Updating or creating a financial plan. It’s crucial to take this step during market downturns as it can provide reassurance that your long-term financial goals are still achievable. Our experience has shown that personal financial plans often remain on track despite market downturns. Take advantage of this opportunity to update your plan and gain some much-needed reassurance.

- Triggering a capital loss strategically if you have non-registered accounts. This can help offset a realized capital gain if you plan to sell an asset, or if you need cash or want to diversify your holdings.

- Lowering the risk profile of your account permanently only if you cannot tolerate market volatility anymore. It may involve selling some holdings at a less-than-ideal time, but taking a hit now could be easier for you in the future. However, this should be considered a final, one-way option.

Reframe your perspective

Imagine thinking about your investment portfolio as if it were your own home. This relatable comparison can help you weather market downturns with greater ease.

Unlike your monthly investment statement, you don’t receive regular updates on your home’s value nor see real estate index numbers fluctuating in real time. This lack of daily stress means that when the value of your home drops, you don’t immediately consider selling it. After all, your home is a long-term investment and a significant part of your net worth.

Similarly, selling off your stocks doesn’t make sense just because the market is down. Likewise, jumping out of the market and buying back once values have risen is not a sound strategy. Instead, stay the course and trust in your long-term investment plan.

Bottom line – We will always have periods of volatility. It’s important to keep calm and avoid knee-jerk reactions that may jeopardize your long-term plan. Review your portfolio and strategies with your Accountant, Financial Planner and Portfolio Manager and gain the confidence you need to stay the course.

Meet Our Team: Holly Harrison, CFP

Holly Harrison is the principal Wealth Management Advisor at Virtus Private Wealth. She brings more than a decade of experience in the financial services industry. She obtained her Certified Financial Planner® designation in 2014. Holly is skilled in building comprehensive financial strategies tailored to her clients’ specific needs. Holly employs a holistic approach to wealth management, helping you building a sound financial plan including insurance, retirement and estate planning.

The post Staying Calm When Markets are Volatile appeared first on Virtus Group.

]]>The post How to Financially Prepare for Divorce appeared first on Virtus Group.

]]>As Jane prepared for divorce, there were so many decisions to be made quickly. She knew she had to be proactive to protect her financial well-being.

Jane first needed to understand her financial situation before entering the divorce process. She started by compiling her financial records – tax returns, loan documents, retirement accounts, bank statements, and investment statements. Then, with her accountant’s help, Jane was able to fully understand where she stood financially.

Jane also pulled her credit report to ensure she knew all her accounts and liabilities. She made a comprehensive list of all her assets that could be divided during the divorce, including their marital home, investments, pensions, personal property, and more.

How Jane Financially Prepared for Divorce

Next, Jane opened new personal bank accounts and closed her joint accounts with her soon-to-be ex-husband. She updated all her direct deposits to her new account and started paying her bills using those accounts. Importantly, to avoid being responsible for any debt her husband may accrue post-divorce, she and her husband agreed to pay off the minimal debt outstanding and closed their joint credit cards.

Jane wanted to ensure her wishes were honoured in the event of her death – and that her former husband wouldn’t have access to her private information. She updated her Will and Power of Attorney, designating new beneficiaries on her investment accounts and insurance policies.

Jane also changed her mailing address to keep her mail private during the divorce proceedings. She wanted to ensure that any correspondence from her lawyer or information about her finances wouldn’t fall into the wrong hands.

Finally, Jane wanted to avoid losing assets or handing over more than she had planned. To do this, she refrained from making significant financial decisions until the divorce was finalized. Instead, she worked with legal and financial professionals to make sure her best interests were protected throughout the process.

Jane had to figure out her new income post-divorce and set a budget. She needed to get her life back on track. With her financial planner, she determined all her monthly inflows, debt payments, and fixed expenses and allocated her discretionary spending accordingly. Together, Jane and her financial planner started a new financial plan and set new, achievable goals. She also reviewed her investments with her portfolio manager to make sure they aligned with her new financial goals and comfort level.

__

Today, with the help of the right professionals, including her accountant, financial planner and portfolio manager, Jane can finally start fresh post-divorce and have financial peace of mind.

Are you at the start, or in the middle of a divorce? Remember these steps.

- Compile your financial records and assess your personal assets.

- Open new bank accounts and credit cards.

- Close joint bank accounts and close or freeze joint credit cards (depending on amount owed, it may be prudent to freeze the credit cards and settle in court).

- Update your Will, Power of Attorney, insurance policies, including beneficiaries.

- Update your mailing address if you no longer live in the marital home.

- Refrain from making significant financial decisions that may be included in the division of property.

Starting Fresh, Post-Divorce

Determine your new income and set a budget.

Post-divorce, your cash flows are likely to change drastically. So first, determine all your monthly inflows, debt payments and fixed expenses. From there, figure out how to allocate your discretionary spending.

Start your financial plan.

Your future looks different than the last time you did a financial plan. Work with your advisor to lay out new objectives and determine the next steps to get your financial life back on track.

Review your investments.

Your investment objectives may have changed since your divorce, or it may be your first time learning about investing. Talk to your portfolio manager and ensure your portfolio aligns with your objectives and comfort level.

Work with your accountant, financial planner, and portfolio manager to clearly understand your financial position and set you on the right path to financial well-being post-divorce.

Meet Our Team: Holly Harrison, CFP

Holly Harrison is the principal Wealth Management Advisor at Virtus Private Wealth. She brings more than a decade of experience in the financial services industry. She obtained her Certified Financial Planner® designation in 2014. Holly is skilled in building comprehensive financial strategies tailored to her clients’ specific needs. Holly employs a holistic approach to wealth management, helping you building a sound financial plan including insurance, retirement and estate planning.

The post How to Financially Prepare for Divorce appeared first on Virtus Group.

]]>The post What is a Trusted Contact Person? appeared first on Virtus Group.

]]>What is the Role of a Trusted Contact Person?

A TCP is a resource that may help protect you in possible circumstances of financial exploitation or where we may have concerns about your ability to make decisions due to physical or mental incapacity. A TCP is also a valuable resource in situations where we are unable to reach you.

We encourage you to provide consent for us to contact your TCP. This consent is gathered in writing at the time the TCP is named. You may also specify restrictions about when your TCP may be contacted.

We may ask your TCP to provide or confirm information, such as:

- Whether anyone may be financially exploiting you;

- Your state of mind if we have reasonable concerns about your ability to make decisions involving financial matters;

- Your current contact information if we are unsuccessful in contacting you after repeated attempts and where failure to contact you would be unusual; or

- To confirm the name and contact information of a legal guardian, executor, trustee, an attorney under a Power of Attorney (POA) or any other legal representative.

Your TCP’s role is to provide or confirm information only – they do not have any authority to make decisions regarding your account and will not be given access to your detailed account information. Your TCP will only be contacted for information where we determine it is absolutely necessary.

Who should you appoint as your Trusted Contact Person?

Your TCP should be an individual who you trust. Typically, your TCP is a family member, close friend, or caregiver.

There is no minimum age requirement for a TCP, however, the TCP should be someone that is mature and able to communicate and engage in potentially difficult conversations with us about your personal situation, including concerns about diminishing capacity.

A client-designated attorney under a POA can be named as a TCP, but you should select an individual who is not involved in making decisions with respect to your account. Your TCP should not be your Financial Advisor on the account.

You may name more than one TCP and may name different TCPs for different accounts.

How is a Trusted Contact Person different from a Power of Attorney (POA)?

A Power of Attorney is a legal document, in which you authorize an individual to make decisions on your behalf should you be unable or choose not to do so yourself.

In contrast, a TCP is essentially an “emergency contact.” Unlike an attorney under a POA, a TCP does not have the authority to make any decision or transact on your behalf.

How do you appoint a Trusted Contact Person?

All clients will be asked to appoint a TCP – both younger and older Canadians can experience health issues that affect their decision making, and both can be victims of financial fraud, including cybercrimes which are becoming increasingly sophisticated.

We will ask you for a TCP when we create a financial plan for you. You should let the person know who you have appointed as your TCP. Feel free to provide them with a copy of this information sheet which explains their role. Please advise us if your TCP has declined the role for any reason.

Although we encourage you to appoint a TCP, if you prefer, you are not required to do so.

You can change your TCP at any time you wish by completing new documentation. If you subsequently name your TCP as a Power of Attorney, we recommend that you appoint a new TCP.

Meet Our Team: Holly Harrison, CFP

Holly Harrison is the principal Wealth Management Advisor at Virtus Private Wealth. She brings more than a decade of experience in the financial services industry. She obtained her Certified Financial Planner® designation in 2014. Holly is skilled in building comprehensive financial strategies tailored to her clients’ specific needs. Holly employs a holistic approach to wealth management, helping you building a sound financial plan including insurance, retirement and estate planning.

The post What is a Trusted Contact Person? appeared first on Virtus Group.

]]>