TAX ALERT | PROVIDED BY RSM CANADA

On Nov. 30, 2020, Canada’s Minister of Finance, Chrystia Freeland, released Canada’s Fall Economic Statement, which represents the federal government’s first fiscal update since before the pandemic. There are several key messages in the government’s Fall Economic Statement.

First, the government provides a summary of the steps it has taken, and will continue to take, to fight COVID-19, including information on the various vaccines purchased and the investment to distribute vaccines.

Second, the government is committed to providing financial support to carry Canadian families and businesses through the second wave of the pandemic. The government recognizes that financial support is still necessary and will do whatever it takes to help Canadians through the crisis. The financial support introduced in the Economic Statement is targeted to the individuals and businesses most affected by the pandemic.

Third, the government will provide a large-scale fiscal stimulus designed to accelerate Canada’s economic recovery, which will be deployed at a time when COVID-19 is under control. The Economic Statement does not release details regarding this large-scale stimulus other than providing it would be an investment of up to $100 billion over the next three years and would build an economy that is greener, more innovative, more inclusive and more competitive. Although these first three key messages relate to spending to get through the pandemic and to facilitate economic recovery after the pandemic, the Economic Statement confirms that unlimited government spending will not last beyond the pandemic.

Fourth, the government identified perceived inequalities in the tax system and proposed specific changes to create a more fair tax system with improved compliance. Such changes include taxing foreign-based businesses selling digital products in Canada (both direct tax and indirect tax), increasing funding to Canada Revenue Agency (CRA) programs targeting international tax evasion and aggressive tax avoidance, and modernizing specific anti-avoidance rules and the General Anti-Avoidance Rule (GAAR).

In the Economic Statement, the government projects a deficit of $381.6 billion for the 2020-2021 fiscal year, with deficits of $121.2 billion and $50.7 billion in the following two fiscal years. The government will release a Federal Budget in 2021.

Following is a summarization of the business and personal income and indirect tax measures in the Fall Economic Statement relevant to the middle market, including international tax considerations, credits and incentives, and audit and enforcement measures.

BUSINESS INCOME TAX MEASURES

The key business income tax measures focus on (1) continuing to support businesses through the pandemic by increasing the potential relief available under the Canada Emergency Wage Subsidy and maintaining the Canada Emergency Rent Subsidy, and (2) implementing the changes to the stock option rules originally proposed in 2019.

No changes are proposed to the federal corporate income tax rates or the $500,000 small business limit.

Increasing the maximum Canada Emergency Wage Subsidy rate

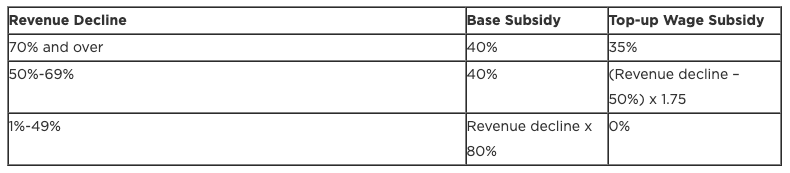

The Canada Emergency Wage Subsidy (CEWS) has provided employers with subsidies in respect of salaries paid to eligible employees since March 15, 2020. Employers are eligible for the CEWS if they experienced a decline in revenue compared to the same month in the prior year (or the average of January and February 2020 revenue). Originally, the maximum subsidy amount was 75% of the eligible remuneration paid to eligible employees (subject to a maximum subsidy of $847 per employee per week). Subsequently, the subsidy was split into a base subsidy and a top-up subsidy, and was gradually decreased. Currently, and until Dec. 19, 2020, the maximum base subsidy amount is 40% and the maximum top-up subsidy amount is 25%, for a total maximum subsidy of 65% of eligible remuneration paid to eligible employees.

In the Economic Statement, the government proposes the following changes to the CEWS:

Support for active employees: The government proposes to increase the maximum wage subsidy rate from 65% to 75% of eligible remuneration paid in the three qualifying periods (periods 11 to 13) between Dec. 20, 2020 and March 13, 2021. The maximum base subsidy would remain at 40% of eligible remuneration paid to employees and the maximum top-up wage subsidy rate would increase to 35% of eligible remuneration as per the following table:

Support for furloughed employees: CEWS for furloughed employees is aligned with Employment Insurance (EI) through Dec. 19, 2020 to provide equitable treatment of such employees between both programs. To ensure that CEWS for furloughed employees remains aligned with EI benefits, the government proposes that the weekly wage subsidy for a furloughed employee from Dec. 20, 2020 to March 13, 2021 be the lesser of:

- the amount of eligible remuneration paid in respect of the week; and

- the greater of $500, and 55 per cent of pre-crisis remuneration for the employee, up to a maximum subsidy amount of $595 (increase from $573 effective for periods 9-10).

Employers can also continue to claim a refund of their portion of Canada Pension Plan, EI, the Quebec Pension Plan and the Quebec Parental Insurance Plan contributions in respect of furloughed employees.

CEWS continues to be a valuable subsidy, especially for businesses severely impacted by the pandemic. Businesses should continue to evaluate whether they qualify for CEWS to offset a portion of their payroll expenses and allow them to maintain employees that they might otherwise be forced to lay off or furlough.

Extending the current Canada Emergency Rent Subsidy and Lockdown Support rates

The government recently introduced the Canada Emergency Rent Subsidy (CERS) and Lockdown Support to provide support to businesses in the form of a partial subsidy of eligible rent expenses, including commercial rent, property taxes (including school taxes and municipal taxes), property insurance and interest on commercial mortgages (subject to limits) for a qualifying property, less any subleasing revenues. When the government introduced the CERS, it detailed the mechanics of the program from Sept. 27 to Dec. 19, 2020 only. Throughout this period, the maximum base subsidy for the CERS is 65% of eligible expenses and the maximum Lockdown Support is an additional 25% of eligible expenses. Lockdown Support is available for businesses that are forced to significantly restrict or cease operations due to a public health order.

The Fall Economic Statement proposes to extend the current CERS base subsidy and Lockdown Support rates for three more periods, from Dec. 20, 2020 to March 13, 2021. As a result, businesses that are forced to close or significantly reduce operations due to a public health order will continue to be eligible to receive up to 90% of their eligible rent expenses (as explained above).

CERS is a valuable subsidy for businesses that have significant rent or commercial mortgage expenses and that are experiencing a revenue decline. In addition, if a business has been subject to full or partial closure due to a public health order, the subsidy is even more significant.

Extension of tax deferral on patronage dividend

Generally, a patronage dividend paid on shares by an eligible agricultural cooperative to its members is taxable to the member in the year in which the dividends are received. The 2005 Federal Budget introduced a tax deferral measure that allows an eligible member of an eligible agricultural cooperative to defer the income inclusion of all or a portion of any patronage dividend received as an eligible share (i.e., a stock dividend) until such time as the owner disposes of the share (including a deemed disposition). The purpose of the deferral was to recognize that cooperative members receiving patronage stock dividends did not receive cash from the agricultural cooperative, thereby making it difficult to fund tax payments thereon. In addition, the eligible agricultural cooperative has no withholding obligations in respect of the patronage dividend at the time of issue of stock dividend and is only required to withhold amounts when the shares are redeemed.

The tax deferral measure introduced in the 2005 Budget applies to eligible shares issued before 2016 and was further extended in the 2015 Budget to cover the shares issued before 2021. The Fall Economic Statement proposes to further extend the tax deferral measure to apply to eligible shares issued before 2026.

INTERNATIONAL BUSINESS INCOME TAX MEASURES

Corporate tax in the digital economy

The government is committed to ensuring that corporations in the digital sector pay their fair share of taxes in respect of their activity in Canada. While the government has a strong preference for a multilateral approach led by the Organisation for Economic Cooperation and Development (OECD), it has expressed concerns about the delay in arriving at consensus. Therefore, in the Fall Economic Statement, the government proposes to impose corporate income tax on foreign-based corporations that provide digital services in Canada, starting Jan. 1, 2022. The details of this new tax are yet to be released, but would appear to work in tandem with the indirect tax proposals relating to digital service and product providers selling into Canada and proposed to become effective on July 1, 2021. This proposal is an interim measure until such time an acceptable common international approach is developed and implemented. The government will announce further details on the temporary measure in the 2021 Federal Budget. For additional information on the taxation of the global digital economy, please see RSM’s previous Tax Alerts on Taxing the gig economy and the OECD’s Pillar One and Pillar Two.

Multinational corporations, especially those engaged in e-commerce, should continue monitoring Canadian and international developments and any potential impacts to their businesses, as jurisdictions are currently adopting a myriad of income and indirect tax measures to address the digital taxation.

CREDITS, INCENTIVES AND OTHER BUSINESS MEASURES

In addition to the temporary COVID-19 relief programs, the Fall Economic Statement sets out several incentive programs to support various industries and communities over the next few years.

Introduction of Highly Affected Sectors Credit Availability Program

Keeping with the government’s approach to target its fiscal support for those most affected by the pandemic, the Fall Economic Statement introduced the Highly Affected Sectors Credit Availability Program (HASCAP). In conjunction with financial institutions, the HASCAP will provide 100% government-guaranteed financing to businesses in highly-affected sectors, such as tourism and hospitality, hotels, and arts and entertainment, at interest rates that are below market. Loans can be up to $1 million with terms of up to 10 years.

The government will soon release more details on the HASCAP.

Support for tourism and hospitality

The Regional Relief and Recovery Fund (RRRF) provides financial assistance to businesses affected by COVID-19. Recognizing that the tourism and hospitality sectors are key economic generators, the government will allocate a minimum of 25% of all the $500 million of RRRF’s resources to support local tourism. Businesses operating in the tourism and hospitality sectors should look to take advantage of this support before the program expires in June 2021.

Extension of rental support for the airline sector

To ensure that Canada’s air sector continues to connect Canadians and Canadian marketplaces, the government proposes to establish several financial assistance programs for both small and large air service providers though various measures, including the following:

- Additional rent relief to the 21 airport authorities that pay rent to the federal government. This support to airports will include repayable and non-repayable rent relief, starting 2020-21.

- Additional financial support to airport authorities in 2021-22 to assist airports with managing the financial implications of reduced air travel.

With ongoing travel restrictions around the world significantly disrupting the airline sector, this assistance can help affected businesses weather the effects of COVID-19.

Green economy incentives

Given the scale of COVID-19 related proposals, there was relatively less focus on green economy incentives. Nevertheless, in line with previous budgets and government statements prioritizing environmental measures, the Fall Economic Statement also provides for selected environmental initiatives, including home energy retrofits, zero-emission vehicle infrastructure and an agriculture fund.

Increased funding for the Strategic Innovation Fund and bio-manufacturing in Canada

In the Fall Economic Statement, the government proposes to allocate $250 million over the next five years to the existing Strategic Innovation Fund to ensure that innovative, intellectual property-rich firms have the support they need to face the challenges presented by COVID-19. Through its continued support of large-scale transformative projects, the Strategic Innovation Fund will help Canada’s most innovative firms and industries weather the pandemic and grow into world leaders that will help drive growth and create jobs in the Canadian economy.

The government also announced a $1.14 billion investment in bio-manufacturing capacity in Canada. This investment includes $193 million for the National Research Council’s Montréal facility, $792 million for the private sector to support made-in-Canada R&D, clinical trials and manufacturing of vaccine technologies, and $150 million for securing equipment and supplies for packaging vaccines.

These investments ensure that Canada is well-positioned to respond to future health emergencies and help promote the long-term sustainability of Canada’s bio-manufacturing sector.

Introduction of Black Entrepreneurship Program

The Fall Economic Statement sets out that Canada will launch its first-ever Black Entrepreneurship Program to ensure equitable access to support and provide opportunities for Black business owners and entrepreneurs across the country to recover from the COVID-19 crisis and grow their businesses.

PERSONAL INCOME TAX MEASURES

No changes are proposed to personal income tax rates, the capital gains inclusion rate or estate tax regimes. However, the Fall Economic Statement provides deductions for employee home office expenses, additional benefits for families with young children and a proposed new tax on “unproductive” houses.

Home office expenses

In light of the vast number of Canadians working from home due to the pandemic, the government proposes to simplify the claim process for individuals to claim home office expenses without burdening the employer to complete Form T2200. Employees will be able to claim up to $400 of expenses, based on the amount of time working from home, without tracking specific costs or retaining receipts. The CRA will release more details in the coming weeks.

Employees that have worked from home in 2020 should see some minor tax relief without having to burden employers for T2200 forms.

First Time Homebuyer Incentive extension

The First-Time Homebuyer Incentive was introduced in September 2019 with the intention of allowing first time buyers to share their borrowing costs with the government. The government proposes to revise this program to make it more applicable in high-priced markets such as Toronto, Vancouver and Victoria. These enhancements include raising the limits on annual income from $120,000 to $150,000 in these markets as well as raising the purchase price allowed from 4 times annual household income to 4.5 times annual household income.

New tax on the unproductive use of Canadian housing by non-resident owners

To help make the housing market more affordable for Canadians, the government proposes to implement a nation-wide, tax-based measure that targets the unproductive use of housing owned by non-residents. The government is committed to ensuring that non-resident owners that simply use Canada as a place to store their wealth pay their fair share of tax. The government will release more details on this new tax in due course.

Non-resident property owners should prepare themselves for a potential “speculation and vacancy” tax, similar to the one that the British Columbia government introduced.

OTHER PERSONAL MEASURES

Support for families with young children

The government proposes to provide support in the 2021 calendar year for families with young children. This support is in addition to a family’s entitlement to the Canada Child Benefit (CCB). Families with household income equal to or less than $120,000 will receive $300 per quarter for each child under six years of age. Families with household income in excess of $120,000 will receive $150 for each child under six years of age.

Investigation into Canada-wide Early Learning Child Care System

The government will investigate the implementation of a government sponsored nation-wide early childhood education and child care program. Finance Minister Chrystia Freeland indicated in her speech that the Federal government would be looking to Quebec for guidance on how to move forward with this initiative.

A national childcare program is unlikely to happen in the immediate future, as the investigations and consultations should take considerable time.

INDIRECT TAX MEASURES

The Fall Economic Statement introduces several indirect tax changes designed to increase fairness and competitiveness between Canadian-based service providers and foreign-based service providers. One of the goals is that Canadian consumers of such products will pay GST/HST to the vendor regardless of the vendor’s jurisdiction and will not have to self-assess GST/HST. An added benefit for the government is to protect the tax base and to help finance government spending for all Canadians.

GST/HST on digital products and services, and operators of platforms that facilitate such sales

Currently, non-resident vendors of digital products and services (i.e., mobile apps, online video gaming, and video and music streaming) who do not have a physical presence in Canada are generally not required to register for, charge or collect GST/HST on sales made to Canadian customers. Rather, Canadian purchasers of these digital products and services are required to self-assess the GST/HST and remit the tax to the CRA, including purchases by individual consumers. Such self-assessment rarely occurs.

The Fall Economic Statement proposes to amend the Excise Tax Act (ETA) to create a new requirement for non-resident vendors of digital products and services to charge, collect and remit GST/HST on sales to consumers located in Canada. In addition, the Economic Statement proposes a new requirement for operators of online platforms that facilitate sales of digital products and services supplied by non-resident vendors (e.g., app stores) to register for, collect and remit the GST/HST on sales made to consumers in Canada through their platforms. The new rules apply to non-resident vendors of digital products or services, and to non-resident distribution platform operators, if the total taxable supplies of such products and services made to consumers in Canada exceed, or are reasonably expected to exceed, $30,000 over any 12-month period.

The proposed effective date for these changes is July 1, 2021. The proposed amendments are similar to the rules introduced for Quebec sales tax purposes that first became effective on Jan. 1, 2019, and follow a trend by the provinces to capture tax on these purchases by businesses and consumers.

To minimize the compliance burden with these new rules, the government proposes a simplified registration and reporting system.

These rules represent a long-anticipated seismic shift for non-residents of Canada who sell digital products and services to consumers or who provide a platform for such sales to consumers in Canada. Coupled with other changes that have taken effect in the last two years or are proposed to take effect next year (i.e., Quebec sales tax, Saskatchewan provincial sales tax, and British Columbia provincial sales tax), non-resident businesses now, or will soon, have significant compliance obligations in Canada. In addition to creating a requirement to register for the tax, businesses will need to determine the rate of tax they are subject to, among other matters.

GST/HST on goods supplied through fulfillment warehouses

Under the current rules, a non-resident vendor who sells goods into Canada through a distribution platform (i.e., a digital platform or online marketplace that facilitates the sales of third-party vendors) and holds inventory in fulfillment warehouses in Canada may not be required to register for GST/HST if the vendor is not considered to be carrying on business Canada. Furthermore, the distribution platform operator is not required to collect or remit the GST/HST on the goods sold through the platform operator’s platform by non-resident vendors in most cases.

The Fall Economic Statement proposes to amend the ETA such that distribution platform operators would be required to be registered for GST/HST once sales of qualifying supplies to consumers (i.e., purchasers not registered for GST/HST) exceed $30,000 over a 12-month period, including supplies made through the distribution platform by non-registered vendors. These measures will apply to supplies made on or after July 1, 2021.

As a registrant under the normal rules, non-resident vendors will be eligible to recover GST/HST paid or payable on purchases and expenses related to their commercial activities by way of ITC.

Duties and taxes will continue to be levied on goods imported into Canada, whether the goods are shipped to a fulfillment warehouse for storage and subsequent sale or shipped from outside Canada to a purchaser in Canada. Goods shipped to Canada directly to an individual, and not intended for commercial, industrial or institutional use, are considered to be a “casual shipment” for customs purposes, and payment of provincial sales taxes (the provincial component of the HST, PST or QST) is typically required to be paid at the border in addition to the duties and GST payable on imports.

These changes to Canada’s sales tax regime regarding remote sellers align with the rules in most OECD countries and finally levels the playing field for Canadian businesses already required to collect and remit these taxes. Remote sellers around the world selling to Canadian customers will have a short time frame to address these changes and adapt to the “new normal” of sales tax in global trade.

GST/HST on short-term accommodation through digital platforms

With the popularity of booking short-term accommodation through digital platforms, there is a potential tax loss compared to traditional accommodation providers. To reduce this tax loss, the Fall Economic Statement proposes that all supplies of Canadian short-term accommodation made through digital platforms will be taxable regardless of the registration status of the property owner. Short-term accommodation involves a lease or license of a residential complex or unit that is rented out to a person for a period of less than one month and for more than $20 per day.

Digital platform operators will be deemed to be the suppliers of short-term accommodation booked using their platform, and will be required to report the GST/HST due on supplies made by property owners who are not registered for GST/HST. This will require the platform operators to register for GST/HST regardless of their residency or whether they are carrying on business in Canada. The platform operator will be required to register for GST/HST if its total taxable supplies of taxable accommodations supplied through the platform to consumers (unregistered persons) in Canada, exceed or are reasonably expected to exceed, $30,000 over any 12-month period.

Non-resident platform operators who are not “carrying on business in Canada” will be eligible for simplified online registration, reporting and remittance options. They will only be responsible for collecting tax on taxable accommodation supplied to persons who are not registered for GST/HST.

Where the platform operator must register under these simplified rules, they are not eligible to claim ITCs; however most charges by platform operators, will not be subject to GST/HST. Any booking or similar fees charged by the platform operator to the accommodation guest, will be subject to GST/HST. Lastly, such platform operators will be required to provide to the CRA certain information about unregistered property owners’ supply accommodation through the platform, as well as maintain records of which property owners provide a GST/HST registration number.

These measures will apply where the consideration for the supply becomes due on or after July 1, 2021, or is paid on or after that day without having become due.

Relief of GST/HST on face masks and face shields

Starting on Dec. 6, 2020, new rules propose to temporarily relieve supplies of certain face masks and shields from the GST/HST (i.e., to make these supplies zero-rated). This relief will continue until public health officials no longer broadly recommend their use in public. The relief will apply to face masks (medical and non-medical) and face shields designed for human use that meet certain specifications. Various methods of construction will be permitted provided they meet the main criteria that the masks or shields are able to prevent the transmission of infectious agents and is not marketed for any other purpose. Masks cannot have an exhalation valve or vent.

As of Dec. 6, 2020, face masks and face shields are exempt from both customs duties and GST/HST. Earlier this year in response to COVID-19, the government issued the Certain Goods Remission Order (COVID-19), which provided relief of customs duty on eligible personal protective equipment (PPE) imported on or after May 5, 2020. Importers of prescribed goods under the ETA should now be able to avail themselves of GST-relieving provisions when accounting for goods with the Canada Border Services Agency (i.e., at time of importation into Canada). However, the requirements for GST/HST relief is more restrictive than the requirements for duty relief. Importers and sellers of this PPE planning to take advantage of the duty or GST relief on importation should confirm the details related to each of the heads of relief when applying for the relief.

AUDIT AND ENFORCEMENT MEASURES

The Fall Economic Statement cites improving tax fairness and strengthening compliance as its key audit and enforcement themes. Specifically, it identifies that the government’s focus is on closing loopholes, eliminating measures that disproportionately benefit the wealthy, and cracking down on tax evasion.

Strengthening tax compliance

Since 2016, the government has provided $350 million per year to the CRA to combat tax evasion and aggressive tax avoidance. These investments target a range of complex tax schemes in areas such as offshore tax evasion and the underground economy.

In the Fall Economic Statement, the government pledges to provide an additional $606 million over five years, starting in 2021-22, to allow the CRA to fund new initiatives and extend existing programs targeting international tax evasion and aggressive tax avoidance. Specifically, the CRA will hire additional offshore-focused auditors to focus on individuals who avoid taxes by hiding income and assets offshore, enhance the audit function targeting higher-risk tax filings, including those of high-net worth individuals.

The government estimates that these measures will increase tax fairness with targeted audits and updated tools to increase compliance, and will generate $1.4 billion in revenues over 5 years.

Modernizing anti-avoidance rules

The government announced that it will explore reworking its anti-avoidance rules. In the coming months, the government will launch consultations on modernizing Canada’s anti-avoidance rules and, in particular, the GAAR. The government’s position is that the anti-avoidance rules are essential to the integrity of the tax system and, therefore, should constantly be updated so they are sufficiently robust for tax authorities and courts to address sophisticated and aggressive tax planning.

The government is taking active steps to tailor the anti-avoidance rules to target sophisticated tax planning. As such, taxpayers should understand the potential risks associated with aggressive tax planning strategies.

Thank you to the following RSM contributors to this content:

Peter Ahn, Senior Director

Sigita Bersenas, Project Coordinator

Dan Beauchamp, Senior Director

Frank Casciaro, Senior Manager

Chi Chen, Manager

David Crawford, Partner

Heather Forbes, Senior Manager

Mariya Honcharova, Senior Manager

Irina Im, Senior Manager

Marino Jeyarjah, Partner

Kenn Jordan, Senior Manager

Nakul Kohli, Manager

Danny Ladouceur, Partner

Manny Lovoi, Senior Manager

Sean McNama, Senior Manager

Yoni Moussadji, Senior Manager

Li Nong, Associate

Jennifer Reid, Senior Manager

Stephen Rupnarain, Partner

Sam Tabrizi, Partner

Chetna Thapar, Associate

Jiani Qian, Senior Manager

RSM Canada LLP is a limited liability partnership that provides public accounting services and is the Canadian member firm of RSM International, a global network of independent audit, tax and consulting firms. RSM Canada Consulting LP is a limited partnership that provides consulting services and is an affiliate of RSM US LLP, a member firm of RSM International. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmcanada.com/aboutus for more information regarding RSM Canada and RSM International.